Traditional claims processing is failing both the customer and the insurer. Here we look at how mobility is helping to forge a new path forward.

Create digital-first experiences fueled by data and customer service to transform the claims process.

In brief:

- While half of all consumers may demonstrate brand loyalty, the proportion of loyal consumers decreases dramatically by generation, with only 37% of Gen Z falling into this category compared to 56% of boomers. To make things even more complicated, Claims is the make- or break-point for any customer relationship, because about 70% of all customer churn in insurance is driven by a bad claims experience.

- The transformation of the claims process is more than just its digitization but requires a customer-centric (re-)design of the process that uses the collection, analysis and integration of data and the integration of technological innovations to not only realize cost and time savings but also drive customer and employee-experience. This allows the carrier to make faster claims decisions and increases transparency toward claims resolution for the customer.

- The new form of mobility and the easy switch between different modes of transportation requires a rethinking from insuring “mere” assets to assuring those mobility journeys. This requires the integration of new technology (partners) and (connected) data sources into the claims experience to take advantage of the insights generated by connected transportation devices drive a better claims experience and reduce claims handling cost. By embracing change, an insurer can transform the claims process from a dreaded experience into an opportunity to build a stronger customer-carrier relationship.

Building trust and retaining younger customers

It’s actually quite simple: Customer service and experience is still king when it comes to building customer loyalty. Capgemini research shows that 67% of consumers claim unpleasant experiences as a reason for switching carriers.

Customer service experiences come into play throughout every insured’s journey. The claims process is the most critical event in the life of a policyholder that ultimately connects the customer and carrier. When the insurer is asked to deliver on its promise to a policyholder/claimant, any break or delay in this fulfillment is at the expense of the customer’s satisfaction and loyalty.

At the same time, the claims organization in particular is currently facing rising costs due to the perfect collision (pun intended!) of internal and external factors. Over the last three years, we’ve experienced a global pandemic, record breaking inflation and endless supply chain disruptions on top of more expensive car parts containing sensors and other new technology, making new cars more expensive to repair and to replace damaged assets. The average number of catastrophic events and nuclear verdicts have also skyrocketed, sending the frequency and cost to settle claims steadily upward.

When we look closely at both customers’ and insurers’ pain points, we see that the traditional claims process is far from perfect. While customers often wait extended periods of time for settlement, carriers incur costs due to delays in communication and settlement. When customers grow frustrated by a lack of transparency in a manual process, carriers often struggle with inaccurate or missing data that could help them make better and faster claim decisions.

This is especially true for the younger generations that have grown up in a world of “everything anytime immediately”; an expectation driven by the digital tools Millennials and Gen-Z are using so natively. This expectation transfer leads to harsh critique of a claim settlement for a insured mobility journey that is delayed or fails to provide relevant and useful status information along the way.

The future is led by data-driven technology

The solution is to transform the claims process by creating digital-first experiences that are fueled by data but enabled by human intervention at the moments that matter.

More than 62% of consumers have continued strong digital habits post-pandemic,and they expect businesses to meet this preference. Self-service channels with back-end automation can speed up claims processing, provide better data and reduce manual touch points while opening up agents to personalize the journey and support them at the critical moments. But that’s just the beginning. The true transformation takes place when claims decisions are enabled by data and insights, and the key are connected devices in cars and other means of mobility that gather useful data when people move from place to place.

With mobility patterns and habits changing because of increased rates of innovation and invention in that transportation space, the way we view coverage and liability will change as well. Consider autonomous cars or shared micromobility vehicles. When done right, mobility data can, in conjunction with the right analytical models, help improve the claims experience for the customer and employees, drive down lost adjustment expenses and even prevent claims in the first place.

Adopt the right technology for your claims strategy

It’s easy to get swept away by the promise of new and innovative technology; the trick is letting the capabilities your organization requires drive the technology you adapt, not the other way around. Even if the insurer has an internal operations or cost goal, a claims transformation should always keep the customer experience at the core.

For example, chatbots are a popular solution for digital customer experiences as they fill a resource gap for the business. These artificial intelligence systems, which can conduct conversations with consumers via text or auditory methods, are used for daily business by more than 40 U.S. insurers. Most online consumers have encountered a chatbot or 20 over the last decade. However, if a company’s chatbot is programmed to assist with anything but the most frequently requested task, the tool is most probably unsuccessful, leaving the customer baffled and frustrated.

With the end-goal and customer journey in mind, the right technology and data ecosystem can be designed for a successful claims transformation, if the following is incorporated:

- Predictive chatbots help reduce barriers to entry for customers using digital intake channels

- Vehicle data from before, during and after an accident help to power new analytical model and speed up claims handling. This includes environmental conditions, traffic information, and information from the site of the accident

- AI/ML models help with accident and damage verification, information verification, completeness checks, fraud detection and intelligent claims assignment

- Generative AI or Knowledge AI support the customer and claims adjuster withtasks likecoverage verification and medical report reviews

- Digital twins for claims and insurers, coupled with augmented reality and virtual reality capabilities, allow for faster claims adjudication and collaboration between various parties involved in an accident

- An API ecosystem allows to connect multiple ecosystem partners with the claims management system

3 questions to guide your future claims strategy — with mobility in mind

Mobility is one of the hottest sectors in insurance driving an eightfold premium growth in the next 5 years. It is expected that within the next decade the mobility ecosystem will itself go through a transformation driven by the rise of ACES (autonomous, connected, electric and shared) vehicles. This will also affect claims transformation efforts already underway as the true impact of mobility on this transformation has yet to be realized.

Here are three questions to guide you through building your future-proof strategy:

- What is our place in a future world of mobility that isn’t necessarily relying on vehicle ownership? How will the increased use of micromobility vehicles like scooters and e-bikes or autonomous cars impact your business? Are the products you offer today fit to serve the needs of this future ecosystem? If not, what products will you need to meet evolving customer trends?

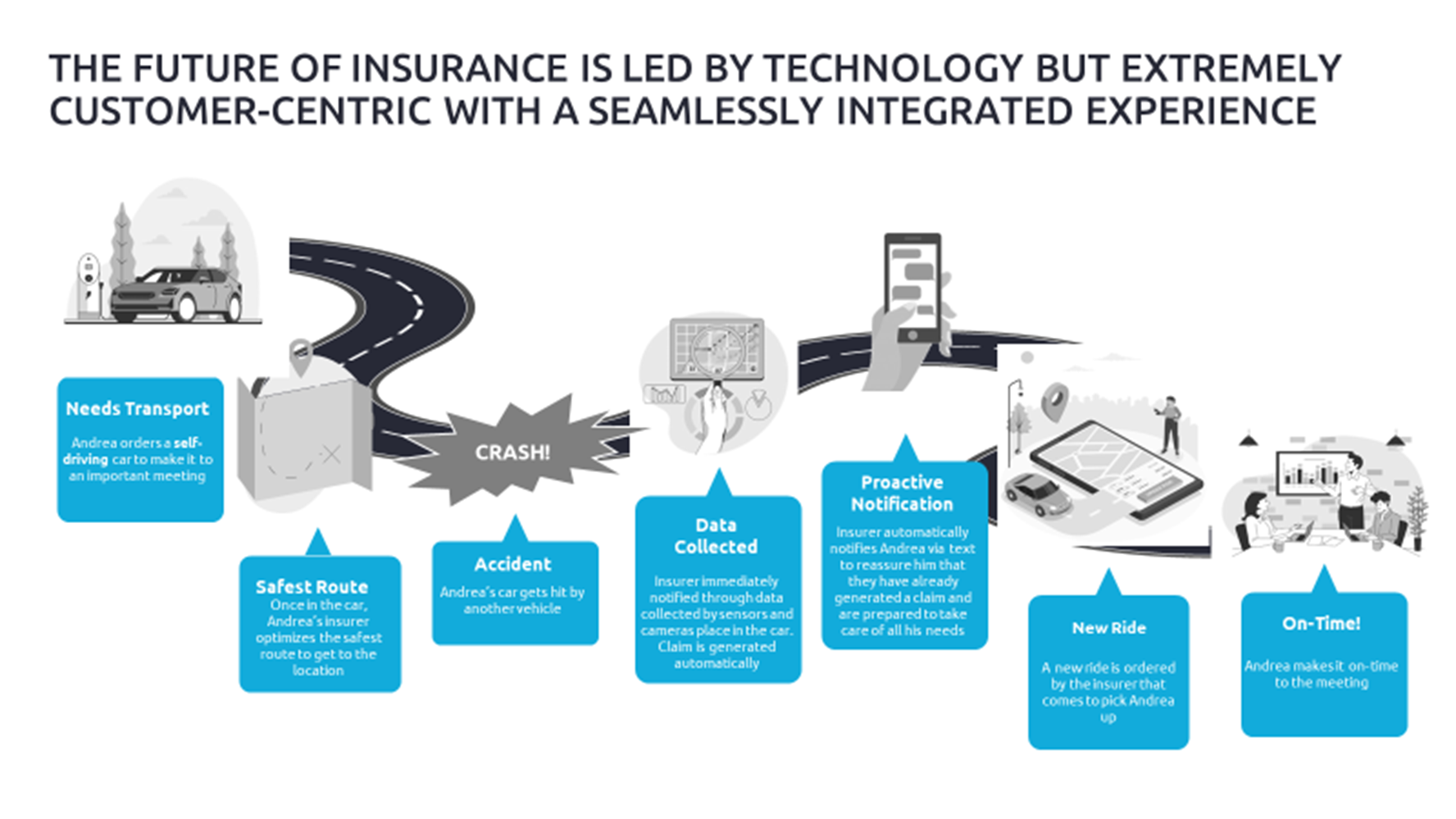

- What is the claims experience we want people to have? Thinking outside of the limitations of the traditional claims journey, what is the ideal experience you can deliver to your customers pre, during and post a claim? How do you want them to feel during the process? If we consider the state of mobility as part of the insured’s journey, the experience starts with the need for transport and extends across a variety of vehicles and touch points.

Identifying the journey and the customer’s needs along the way allows you to reverse plan and answer the question what data and capabilities will you need to deliver a seamless and integrated experience?

- How do we best distribute our products? Insurtech and embedded insurance is bringing the point of sale directly to the consumer when and where coverage is needed. Consider the e-bike. When a user arrives to rent the bike, can your product be embedded in the renting experience at the point of sale? What innovative ways can you deliver your product to the consumers when they need it most?

In conclusion

Any true transformation takes time, and the journey will be different for each carrier based on their existing operations and customer needs. Change management is a huge piece of the puzzle, and often a deterrent. But by embracing change, an insurer can transform the claims process from a dreaded experience into an opportunity to build a stronger customer-carrier relationship.

Capgemini has a human-centered approach to creating a Future of Claims strategy, experience and roadmap that focuses on building the relevant capabilities for your business and goals. Learn more about our approach in our Future of Claims Point of View.